The degree of uncertainty in today's market can make pin pointing the correct entry point fairly difficult at times, but while economic headwinds continue to force stocks to experience large pull backs, investors will have plenty of buying opportunities in the near-term. Recently, I came across Buenaventura Mining ( BVN), or if you must, Compania de Minas Buenaventura, a small, yet well diversified mining company that's heavily involved the exploration of precious metals. While mining activities do make up the core of its business, it also generates a second stream of income from the electrical utility services it provides to outside mining companies. Buenaventura's split business menu offers shareholders a sufficient level of diversification in terms of risk, but just like anything else, there are a number of risks that can simply not be avoided.

Over the last 12 months, Buenaventura's security price took a nasty turn along with many other mining companies in and outside of the United States. This negative performance can be primary attributed to the price decline of metals in commodity markets. Above others, gold experienced the largest drop in price, which ultimately led to serious margin compression for mining companies across the board. Generally speaking, 2013 was a horrible year for mining companies, and while valuations continue to remain low, the beginning of 2014 will be an excellent buying opportunity. Not only is Buenaventura extremely cheap based on the underlying resources at its disposal, but its shares are trading at a 20% Discount to its per share book value. The uncertainty pertaining to the risks that forced its stock price into the slums still exists, however, the high level of price volatility in commodity markets that previously existed does not. The reduced level of volatility has already allowed metal prices to start recovering, and consequently, this will stimulate margin growth. Improving economic conditions along with this hefty discount have created a short-term buying opportunity that's quite intriguing.

BackgroundHeadquartered out of Peru, Buenaventura holds a dominant position with over 60 years of experience in the mining industry. The combination of having an experienced management team, equity investments in properties containing lucrative resources, and a strong portfolio of mining projects has allowed Buenaventura to become Peru's largest publicly-traded precious metal company. Today, its operations are comprised of two business segments, including mining and the specialized set of utility services it provides to other mining companies. On the mining side of its business, Buenaventura is physically engaged in the mining process, development, and exploration of a various metals such as gold, silver, zinc, copper, lead, and copper.

Geographically speaking, the location of its operations is very diverse, but most importantly, it provides a degree of isolation from competing firms. As for ownership, these properties are either wholly owned or partially owned through an equity stake that gives Buenaventura either controlling, or in some cases, minority interest in the property. The properties that are wholly owned by Buenaventura include Orcopampa, Uchucchacua, Poracota, Antapite, Julcani, Recuperda, Shila-Paula, and Malla. The properties for which it has controlling interest are La Zanja, Tantahuastay, Colquijirca, ad Marcapunta. One of the most prominent gold mines in Latin America is Yanacocha, which Buenaventura has 43.65% of minority interest via a partnership with Newmont Mining Corp ( NEM). Additionally, Buenaventura has minority interest through its equity investments in Cerro Verde and Chucapaca. The stakes in both of these properties are 19.58% and 49%, respectively. As you can see, there is an extensive amount of mining properties in Latin America, and while these exist, the rise of competitive threats across the industry are inevitable.

Currently, Buenaventura is faced with a handful of competitors, however the aggregate level of competition is much less than you would think. By being the sole owner on multiple different properties, Buenaventura has access to a variety of metals that many other firms do not have access to. Therefore, Buenaventura is capable of minimizing competition from this angle, and can direct its focus on how it will manage the competitive threats that derive from other firms having access to the properties in which it only has controlling or minority interest. And given Yanacocha is one of the top locations in this region for mining gold, it's easy to see that Buenaventura's partial stake in this property means that its not the only firm capable of utilizing the resources at this location to turnover an economic profit.

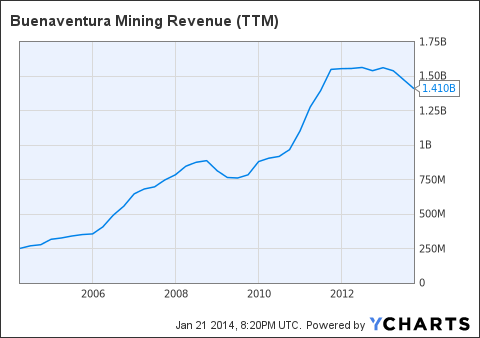

Commodity Price Volatility, Margin Compression, & Increased UncertaintyWhile the fluctuations in Buenaventura's stock price has created a tremendous amount of uncertainty going forward, its operating history provides investors with a much higher level of reassurance. And even though there are several concerns pertaining to Buenaventura's margins specifically, the industry as a whole has seen compression across the board, which makes this a minor concern going forward. Before we take a look at how the volatility in commodity prices has impacted the margins for mining companies, we need to evaluate Buenaventura's ability to turn over a profit. For starters, let's take a look at Buenaventura's revenue:

BVN Revenue (TTM) data by YCharts

As we know, Buenaventura operates two business segments that provide separate streams of income. Therefore, it's important to recognize that the vast majority (roughly 70%) of its revenue derives from precious metals. With the exception of stagnant revenue growth in 2012 followed by an unattractive decline of 2013, you will notice the average level of revenue in these two years is still more than 6x what it was in 2004. While the general consensus of sell-side analysts expects that its revenue will see strong growth over the next two years, its revenue however does still appear to be trending downward, which indicates there's a favorable probability that it will continue to decline in the short-term. On a positive note, the price of gold is beginning to make a recovery, and parallel with this price movement, we will see improvement in Buenaventura's margins.

Gold Price in US Dollars data by YCharts

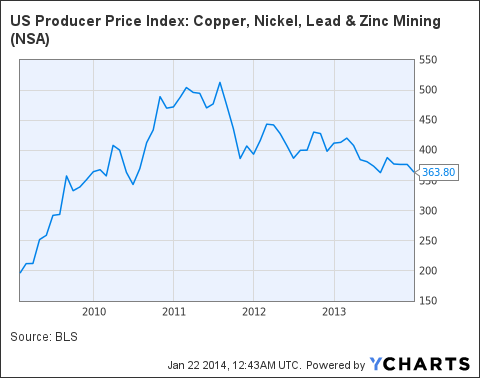

Above, it's easy to see that the aggressive sell off of gold in 2013 created a horrible economic environment for mining stocks. Even though we did see a small pull back in Buenaventura's total revenue, the lower price for commodity metals such as gold had a far worse effect on its margins, which you will see shortly. In order to evaluate the other economic variables that contributed to the decline in margins for firms such as Buenaventura, let's take a look at the performance of the US Producer Price Index. This index consolidates the price fluctuations of four different metals into one numerical measure. Also, it's important to note that all of the metals included in this index are the same metals that Buenaventura mines for at its properties.

US Producer Price Index: Copper, Nickel, Lead & Zinc Mining data by YCharts

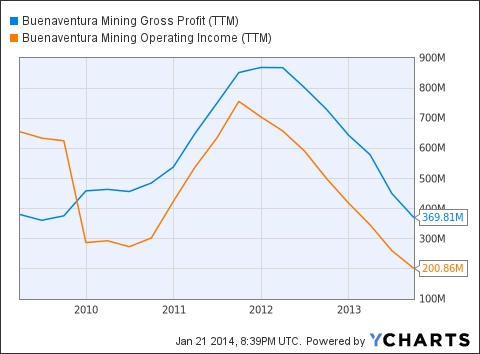

With the large fixed costs required to complete mining projects, this industry can be fairly capital intensive at times. So, this is clearly not the first time Buenaventura has experienced margin compression, but based off the recent decline in its gross and operating income below, it does appear to be one of the worst cases it has seen. In terms of its relative performance from 2013 to 2014, its gross and operating profit declined by approximately 36% and 41%, respectively.

BVN Gross Profit (TTM) data by YCharts

Consequently, margin compression also has influencing control over the final EPS figure, and unfortunately, its EPS have moved in the same direction as the other metrics we have seen. For the fiscal year ending 2012, its final EPS figure was $2.67, and although its final EPS figure for 2013 has yet to be released, its TTM average at $1.27 suggests there has been a significant YoY decrease. On a QoQ basis, there does not appear to be any cyclical components within this industry's business cycle that would create a notable change in earnings one quarter over the other. With the exception of the slight recovery commodity prices have seen, there is nothing significantly different that would lead us to believe the EPS figure in the 4th quarter can offset the damage that was previously done this year.

It's important to understand that even though its EPS have declined, there is nothing fundamentally wrong with Buenaventura's business that would deteriorate the solid value its shares offer in the market. Internally, its cost structure remains consistent with previous years, which tells us the margin compression it has experienced is directly tied to the price movements for commodities over the last year. Margin compression is something you will never find on a long investor's wish list, however you will find that investor's perceive the source of Buenaventura's margin compression highly attractive over it sourcing from an internal issue pertaining to its cost structure. Across the board, Buenaventura displays a very low level of both, operating and financial leverage. And although its level of debt caters to maintaining a higher degree of financial leverage than operating leverage, the risk from this angle going forward is minimal. Overall, the decline in Buenaventura's margins did merit a sell off, but given the price drop, the extent to which shares were sold off was exaggerated.

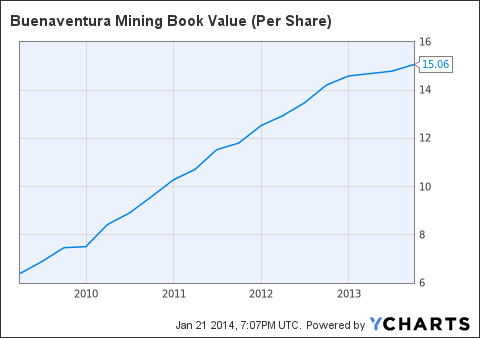

Shares are Cheap, but How Exactly Will its Asset Valuation Be Impacted in the Future?Right off the bat, looking at Buenaventura's book value makes it quite easy to understand its shares are undervalued. Trading just above $13 per share, the spread between its book and market value stands at roughly 20%. This current discount offers an attractive entry point for investors, but more importantly, the growth its book value has seen is far more intriguing. For the last five years, Buenaventura's book value has grown by about 30% on an annual basis, which is quite impressive. Since the start of 2013, you will see above that its book value has continued to grow, but at a considerably lower rate.

BVN Book Value (Per Share) data by YCharts

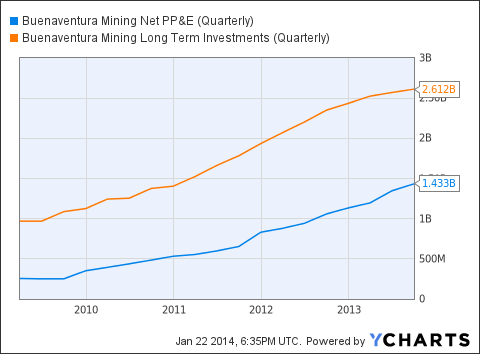

Buenaventura will continue to be an attractive short-term play while it shares trade below book value. However, as this gap becomes closer to being obsolete, reevaluating the economic conditions regarding metal prices will be essential for determining what will drive the valuation of its shares up or down. With that being said, we can already assume that commodity prices will have a fair influence on the value of its core operating assets. However, the second main driver can be controlled internally. Specifically, it will pertain to the strategic decisions management makes in regards to how it plans to preserve and grow the value of its core asset set going forward. Before getting into the specifics of decisions management has at its disposal, let's take a look at core assets. Within the non-current assets on its balance sheet, there are two account balances we need to analyze, which include (1) Net property Plant & Equipment, and (2) Long-term Investments, or also known as, Equity & Other Investments. Based on the chart below, it's clear that management has done an effective job in building a fine set of assets. From the graph below it's difficult to tell, but for the period ending September 2012, or Q3, Buenaventura's Net PP&E and Long-term investments were roughly $1.058bn and $2.351, respectively. In just 12 months, these non-current assets accounts saw astonishing growth by 35% and 11%, respectively.

BVN Net PP&E (Quarterly) data by YCharts

Generally speaking, economic conditions do have a strong pull over the performance of these assets, and for mining companies in particular, reduced price levels for commodities often result in the valuation being negatively impacted. But as you can tell, the valuation of Buenaventura's assets are not heavily correlated with the commodity prices. The valuation of its Net PP&E saw approximately the same growth in line with previous quarters, however its long-term equity investments did not increase as much over the last 12 months as we've seen in previous years. From an investment standpoint, this is highly attractive, and going forward, it's relatively safe to say that Buenaventura's assets are not too heavily impacted by commodity prices. With that being said, investor's are in a sound position because as commodity prices rebound, asset valuation will go up across the board. Therefore, management now has an opportunity to take advantage of these low price levels.

As mentioned earlier, there are multiple things that management can do to that will allow them to strategically capitalize on this short-term window of opportunity, and ultimately, augment the value of the firm. Internally, there are a wide range of possibilities, but in this industry, acquisitions are by far the most common. And with commodity prices as low as they are today, acquisitions can be very advantageous. Investors would greatly benefit from an asset purchase either via a firm whose choosing to discontinue its operations, or from a pure acquisition of a smaller competitor. In the case a transaction a such were to occur, Buenaventura's book value would see a strong increase in the short-run, and in the long-run, it would increase the potential for what its book value could ultimately reach. Right now, management has no disclosed any information regarding potential acquisitions, however there's a good chance we may see one take place as commodity prices take a full recovery. By management waiting for commodity prices to recovery prior to making an asset purchase or acquisition, it reduces the burden and risk associated with acquiring assets that could diminish in value if economic conditions were to worsen.

RisksAs we saw earlier, the health of Buenaventura's revenues are heavily correlated to the price performance of metals in commodity markets, and with a cost structure that's been highly stable, the final revenue figures on the income statement will be the most influential driver in terms of valuation. Thus, the largest risk at stake will continue to be the performance of commodity markets, and specifically, the positive or negative price movements of metals in the near-term.

Relatively speaking, the percentage decrease we saw in the price of metal should not be used as a comparable for estimating the percentage change in revenue. At the beginning of 2013, gold was selling for close to $1,700 an ounce, and by the end of the year, the selling price decreased by about 36% to $1,250. During this same period, revenue decline by only 11%, yet its shares dropped over 60%. While we do not have any real comparable data to go off of, we do know revenue needs to bounce back to previous levels, and the price of gold needs to makes a strong recovery. Regardless of when these events take place, we do know Buenaventura was able to maintain its book value, and actually, improve it within the last year. Going forward, investors should monitor the price fluctuations of metals in commodity markets closely, and watch for changes in revenue. As long we see a recovery in metal prices, the change in revenue should be favorable.

Final ThoughtsThe discount Buenaventura's shares offer is quite transparent, and without even factoring in the revenue growth Buenaventura is bound to see when commodity prices adjust, the upside potential is still attractive. As I've clearly established, the largest driver going forward is the recovery we are going to eventually see in commodity markets, and the potential value that will be added through the excess revenue generated during this recovery period. Historically speaking, gold and silver have proven to be extremely volatile investments that have not properly corresponded normally to inflation. Right now, there are numerous analysts anticipating that gold and silver will follow a more normalized inflation schedule starting within the next year, and in the case this where to be true, valuations of firms in the mining sector would receive a strong boost. Conclusively, the mining sector is experiencing some of the lowest valuations we have seen in a while, and while Buenaventura continues to trade at an extreme discount, it's now an excellent time to capitalize on its common shares.

No comments:

Post a Comment